As part of the recently signed Consolidated Appropriations Act of 2021 the Paycheck Protection Program has reopened with funds available for new loans for both new and repeat borrowers. In addition, the law has extended (and modified) other benefits that were previously set to expire at the end of 2020 - these include paid leave credits for Covid related illness, along with Employee Retention Tax Credits.

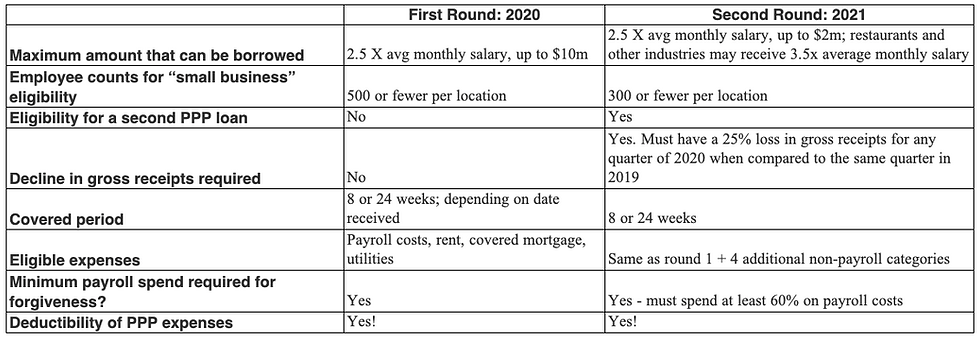

Second Time PPP Borrowers

Second PPP loans are available but requirements to qualify are much more restrictive than the first time around. Businesses must be able to demonstrate:

-

A reduction in revenue of at least 25% between corresponding quarters in 2020 and 2019.

-

Borrowers must have fully spent the loan proceeds from their first PPP loan before their second PPP loan is disbursed.

-

They must have 300 or fewer employees.

Consistent with the first round of PPP, 100% of the amount received can be forgivable as long as the proceeds are spent in accordance with program rules. Check the Small Business Administration’s PPP website for more information. Non-payroll costs remain limited to less than 40% of the loan amount or, in other words, you must spend at least 60% on payroll costs. Additionally, for all borrowers who have not yet applied for forgiveness, the safe harbor deadline to restore wage and employment levels is extended from December 31, 2020, to September 30, 2021.

Highlights of PPP Changes are summarized in the table below:

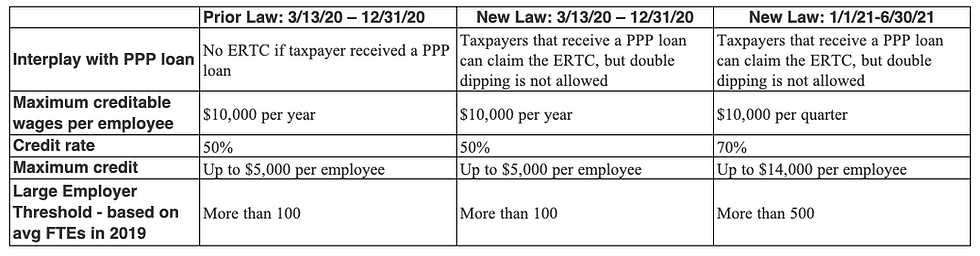

Extension of Employee Retention Tax Credit (ERTC)

As of January 1 2021, the Act increases the credit rate from 50% to 70% of qualified wages, increases the per employee wage cap from $10,000 in the aggregate to $10,000 per calendar quarter, decreases the required decline in gross receipts from 50% to 20%, and increases the threshold for treatment as a large employer from 100 employees to 500 employees. Can you claim the ERTC if you receive a PPP loan? Yes! In previous version of Covid related regulation, this was not allowed. However, one of the most favorable provisions in the new law allows taxpayers to both receive PPP loans and claim the ERTC. As a result, businesses that received PPP loans in 2020 and / or 2021 can now explore potential ERTC credits for both 2020 and 2021. We anticipate more guidance on reporting retroactive changes for 2020, which likely will require amendments on 2020 941’s or an additional filing. We are awaiting further IRS guidance and working with your team to determine how to account for these credits. Can pay for wages with PPP loan proceeds AND claim the ERTC too? No. Wages used to claim the ERTC cannot also be counted as payroll costs for purposes of determining the amount of PPP loan forgiveness. In short, you cannot double dip on benefits simultaneously.

Highlights of the ERTC changes are summarized below:

Extension of Paid Leave Credits

The FFCRA required employers with fewer than 500 employees to provide mandatory paid sick and paid family leave for certain reasons related to COVID-19 and a corresponding tax credit. New legislation extends the tax credit portion of the FFCRA for employers that voluntarily offer paid sick or paid family leave through March 31, 2021. The limits on wages paid still apply. These credits are essentially government funded paid sick leave for employees that cannot work due to Covid related circumstances.

To better understand your options, please feel free to contact Paysteady to speak with one of our payroll specialists!